Roof Insurance Claim in San Antonio

Filing a roof insurance claim in San Antonio? See your exact replacement price first — in under 2 minutes. Walk into the adjuster meeting with a real number, not a guess.

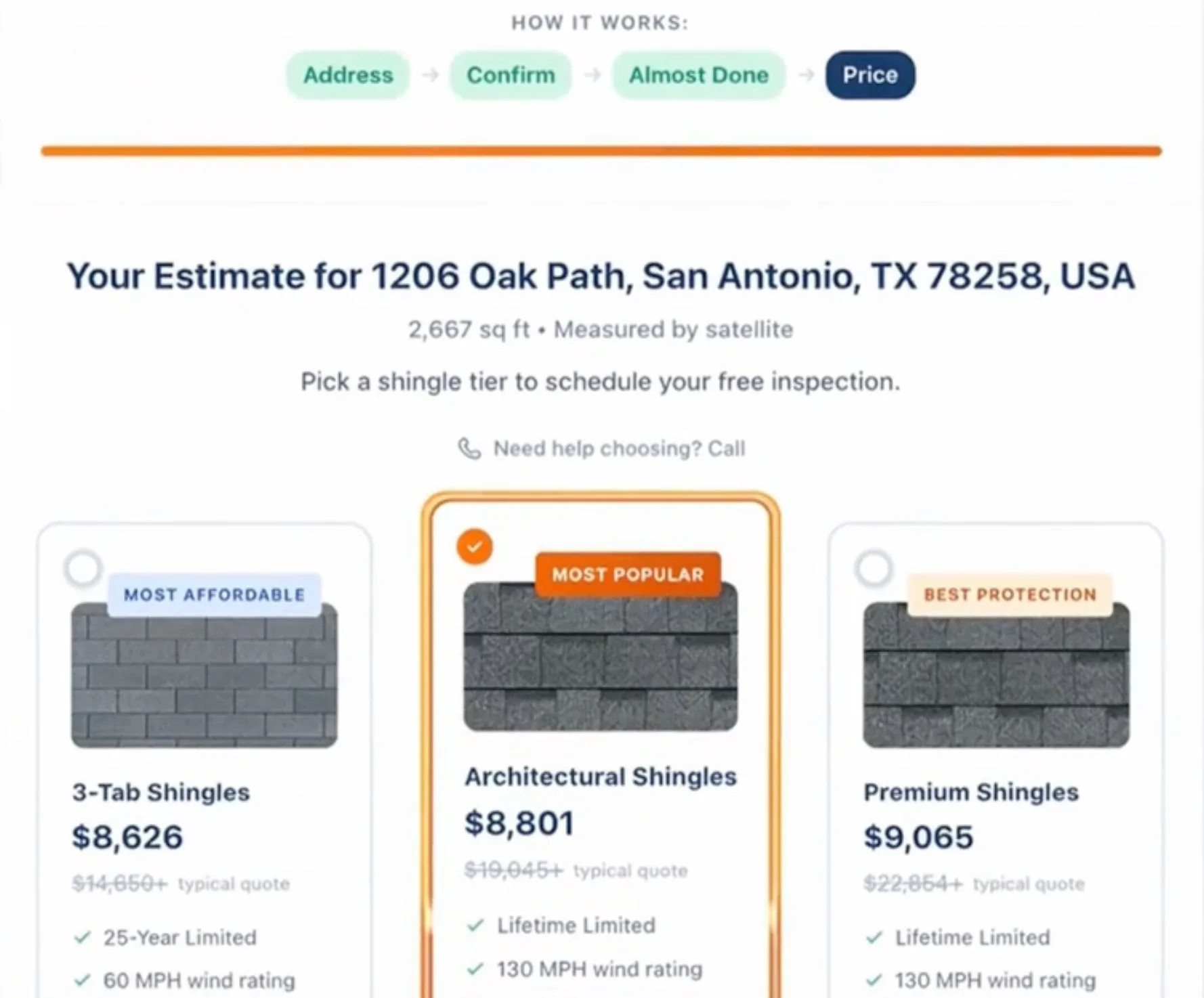

Save 40-50% — See Your Instant Price

- ✓ Same Owens Corning shingles

- ✓ No sales commissions or franchise fees

- ✓ Instant quote — no home visit needed

Know your replacement price before you file

Most homeowners file an insurance claim without knowing what their roof replacement actually costs. They rely on the adjuster's number — and adjusters work for the insurance company, not for you.

This page is for storm-damaged roofs. If your insurer is non-renewing you because your roof is simply too old — not damaged — start there instead.

Whether your roof took hail damage, storm damage, or wind damage, here's a better approach:

- See your price first — enter your address in our estimator and get your exact replacement cost in under 2 minutes. No appointment, no obligation.

- Use that number with your adjuster — when the adjuster visits, you'll know whether their assessment is fair. If their number is lower than your actual replacement cost, you have documentation to push back.

- Avoid underpayment — insurance companies routinely underpay roof claims. Homeowners who know their replacement cost before filing get better outcomes.

We also help with the documentation. We provide detailed damage reports with photos that your adjuster can use — and we'll meet with your adjuster on-site if needed.

Why the deductible math has shifted

Filing a Texas roof insurance claim today is a different decision than it was a decade ago. The numbers have moved:

- Average wind/hail deductible: ~$8,000 on a $400,000 San Antonio home (2% of dwelling coverage). Larger homes face $10,000-$14,000 deductibles.

- 47% of Texas homeowner claims are closed without payment, up from roughly 35% a decade ago, per Texas Department of Insurance data.

- Premiums have climbed 55% since 2019 — the average Texas homeowner premium reached $3,291 in 2024 and is projected to hit $4,529 by the end of 2026.

- The Texas FAIR Plan — the state's insurer of last resort — has grown from 66,500 policies in 2021 to over 121,600 by early 2025 as more carriers pull back from hail-zone underwriting.

- Older roofs face ACV depreciation — major insurers increasingly apply Actual Cash Value to roofs over 10-15 years old, plus cosmetic damage exclusions and "scheduled roof" endorsements that age out coverage.

This doesn't mean don't file. It means do the math. If your deductible is $8,000 and our direct-pay price for your home is $11,000 — with no denial risk and no premium increase waiting on the other side — that changes the decision. Many homeowners still file, and we handle insurance claims when they do. But direct-pay is now a real option, not a desperation move.

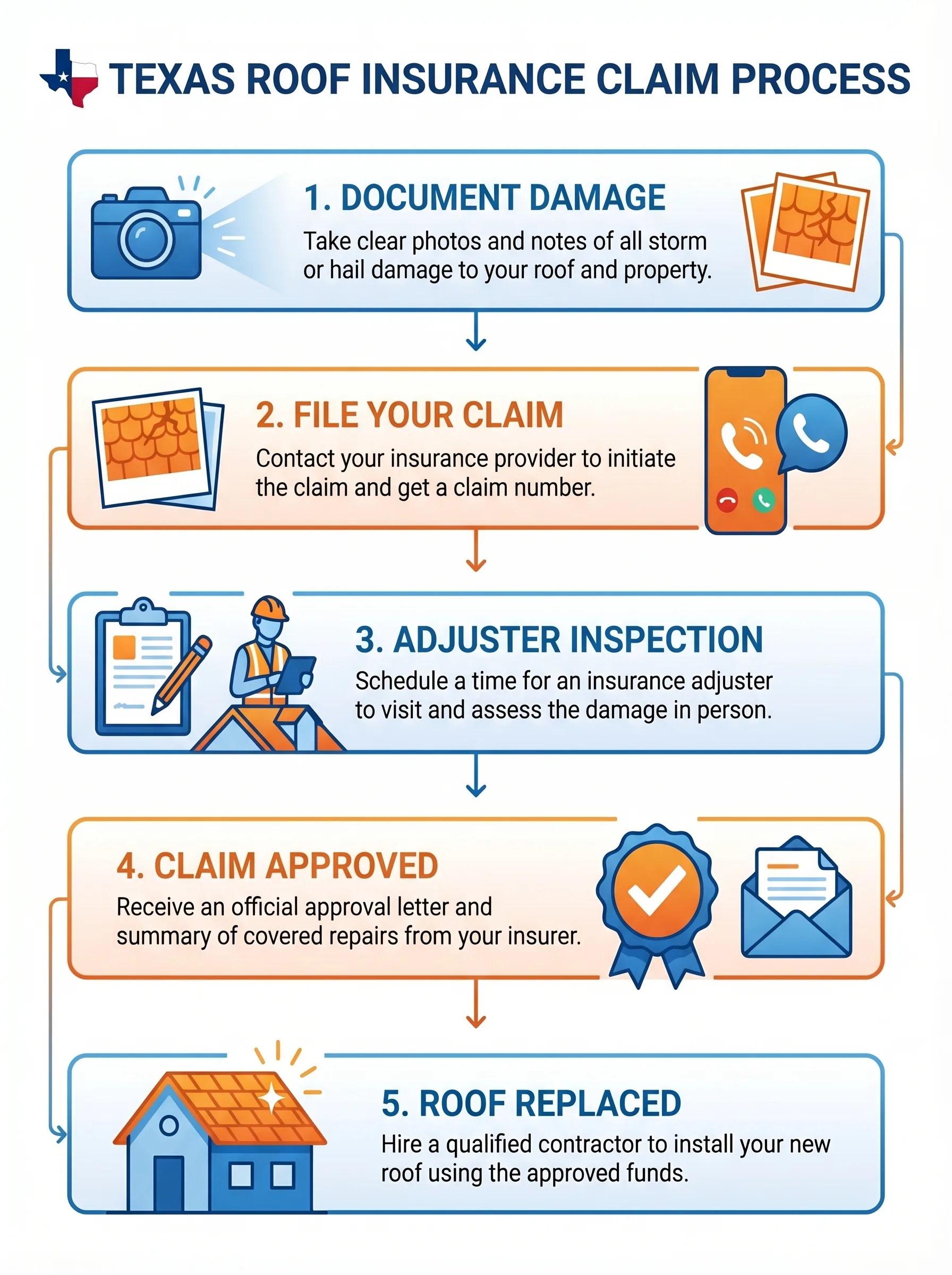

How the roof insurance claim process works in Texas

The Texas roof insurance claim process has five steps:

- Document the damage — take photos of your roof from the ground, check gutters for granule buildup, photograph any interior water stains. Do this immediately after the storm.

- File your claim — call your insurance company and open a claim. You'll get a claim number. In Texas, most policies require filing within one year of the damage date.

- Adjuster inspection — your insurance company sends an adjuster to assess the damage. This is where knowing your replacement price matters — you can compare their assessment to your real number.

- Claim approval — if approved, your insurer issues payment based on your policy type. RCV (replacement cost value) policies pay the full replacement cost minus your deductible. ACV (actual cash value) policies deduct depreciation based on roof age — which can cut payouts on a 15-year-old roof roughly in half. Most insurers pay in two installments: a partial payment up front, with the recoverable depreciation released only after the work is complete and you provide proof the deductible was paid.

- Roof replaced — choose your contractor and schedule the work. With Roof Direct SA, your out-of-pocket cost is typically just your deductible — and our prices are 40-50% lower than the big companies, which means more of the claim goes toward your new roof.

What to do if your claim is denied

A denied claim doesn't mean the conversation is over. In Texas, you have options:

- Request a re-inspection — ask your insurance company to send a different adjuster. The first adjuster may have missed damage that's only visible at roof level.

- Get a professional inspection — a detailed damage report from a licensed roofer gives you evidence the adjuster didn't have. We provide these at no cost.

- File a complaint with TDI — the Texas Department of Insurance (800-252-3439) accepts consumer complaints and investigates unfair claim denials.

- Consider a public adjuster — a public adjuster works for you, not the insurance company. They re-assess the damage and negotiate directly with your insurer.

Don't let a denial stop you from protecting your home. Many denied claims are overturned with proper documentation and a second inspection.

Is it legal for a roofer to cover my deductible?

After major San Antonio storms, homeowners are routinely approached by roofers offering to "absorb," "waive," or "work around" the insurance deductible. This practice is illegal in Texas.

Texas Insurance Code §707.002, enacted under House Bill 2102 in 2019, makes it a Class B misdemeanor — punishable by up to 180 days in jail and a $2,000 fine — for a roofing contractor to advertise that they will pay, waive, or absorb the homeowner's deductible. The law applies to both the contractor and any homeowner who participates.

Insurers may also legally refuse to release the recoverable depreciation portion of your claim until you provide proof the deductible was paid. The waived-deductible offer often comes paired with an inflated quote — the "savings" is fictional, and the homeowner can end up with an unfinished job, a denied final payment, and exposure to the misdemeanor charge.

You can report fraudulent practices to the Texas Department of Insurance fraud unit at 1-800-252-3439.

Our roof replacement in San Antonio pricing is published before any conversation happens. There's no inflated quote to work backward from — if your insurance pays, the claim pays toward our published price. If you pay direct, you pay the same number. Either way, the price is the price.

Frequently asked questions

Roof damaged? See your price now.

Enter your address and get your exact roof replacement cost in under 2 minutes. No appointment, no salesperson.